Trading and Risk Software. Delivered.

CompatibL is a leading provider of custom software development services, trading and risk management software solutions, cloud services and solutions and model validation consultancy for the financial industry.

CompatibL’s unique strength lies in combining advanced application engineering with industry-leading quant expertise to deliver best-in-class software solutions for banks and asset managers.

Whether it’s custom banking software development services, cloud financial solutions, trading and risk software or model validation — we have you covered from concept to delivery.

We offer a powerful combination of complex tech and detailed quant expertise, advanced processes, and proven experience in implementing trading and risk management solutions to financial institutions worldwide.

CompatibL is a leading provider of custom software development services, trading and risk management software solutions, cloud services and solutions and model validation consultancy for the financial industry.

CompatibL’s unique strength lies in combining advanced application engineering with industry-leading quant expertise to deliver best-in-class software solutions for banks and asset managers.

Whether it’s custom banking software development services, cloud financial solutions, trading and risk software or model validation — we have you covered from concept to delivery.

We offer a powerful combination of complex tech and detailed quant expertise, advanced processes, and proven experience in implementing trading and risk management solutions to financial institutions worldwide.

Risk Market Technology Awards 2025

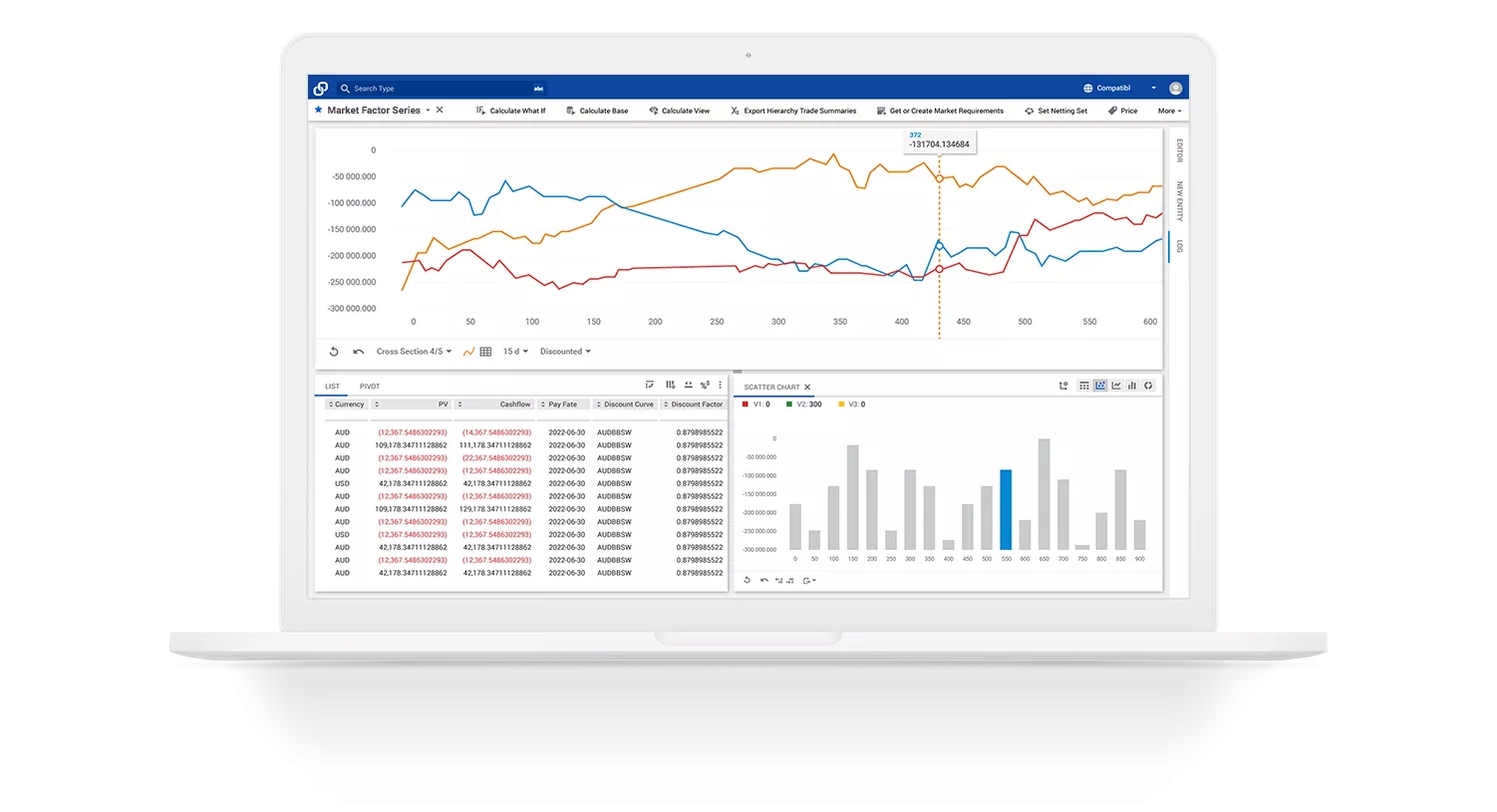

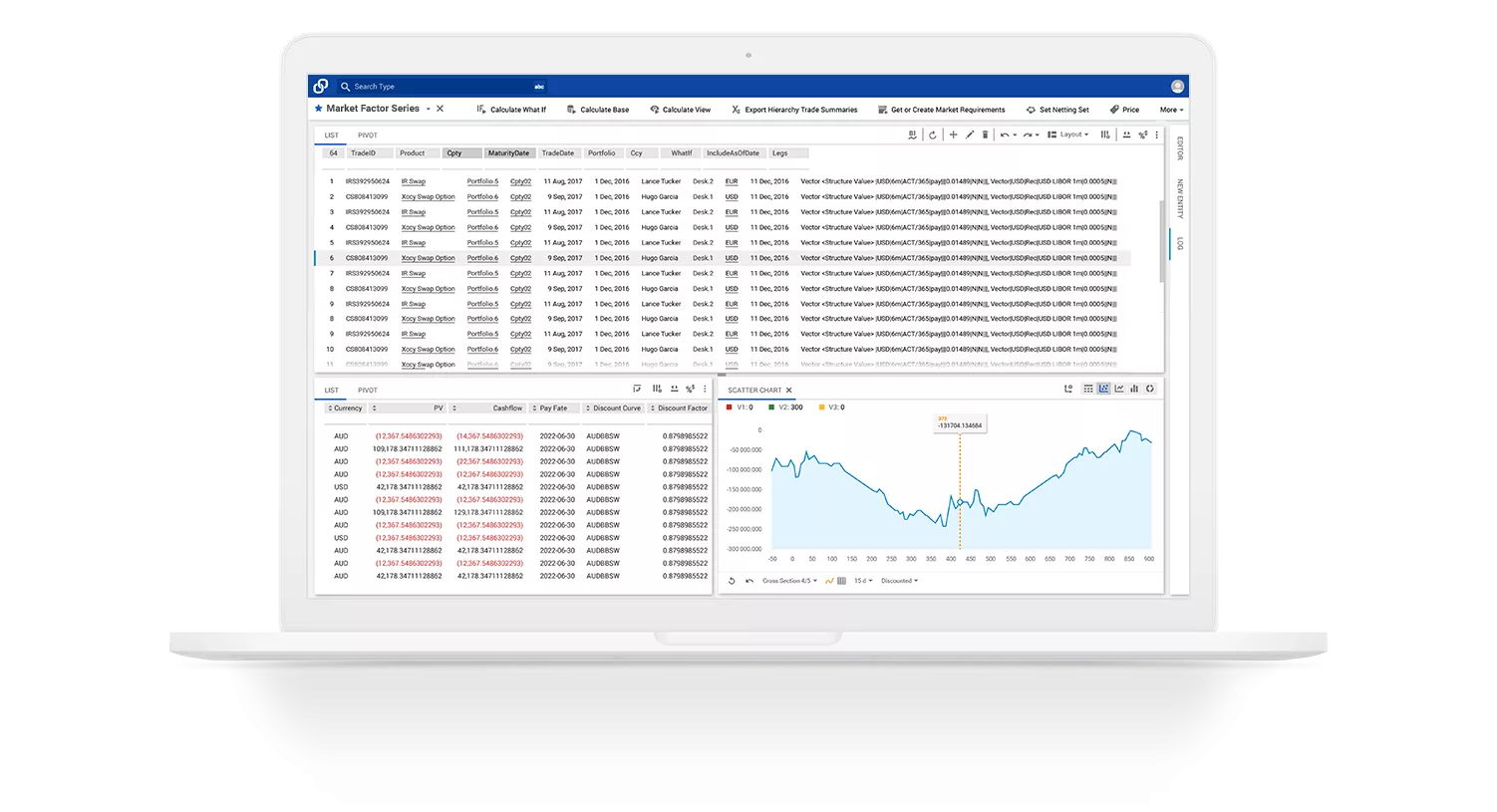

Discover CompatibL’s award-winning solution for AI-driven trade entry for what-if analysis.

Learn practical techniques for measuring

and mitigating AI risk.

No coding required.

Learn about the benefits of deploying large language models in the financial sector, exploring their application in day-to-day operations, model governance, and the challenges of implementation.

Alexander Sokol’s working paper “Autoencoder Market Models for Interest Rates” has been published on SSRN. Click the button below to get the full version of the paper and learn more about the new type of interest rate models based on machine learning.

Trading and Risk Management Software

CompatibL AI for Quant Finance

Financial Software Development

Cloud Services and Solutions

Regulatory Compliance Services

Our Customers Say

About CompatibL

A trusted partner

As a trusted business partner to major banks and commercial finance companies, CompatibL provides secure, compliant solutions that meet customers’ requirements.

CompatibL is SOC 2 Type 2 certified and undergoes regular SOC 2 audits to maintain compliance with the latest security recommendations.